Why a Year-End Financial Review Is So Important

The final months of the year are often a whirlwind of festivities, family gatherings, and gift-giving. While it's a season of joy, it can also bring significant financial pressure. Many people find themselves swiping credit cards more frequently, resulting in a new year that begins with a mountain of holiday debt.

Think of Q4 as your financial fourth quarter. It’s the ideal time to look back on your spending habits, see how close you are to your goals, and make any necessary adjustments. A thorough review helps you prepare for tax season, refine your budget for the upcoming year, and prevent the kind of impulse spending that can lead to long-term setbacks.

This guide offers a comprehensive checklist to help you navigate the holiday season without derailing your financial goals. From practical holiday budgeting tips to long-term debt payoff strategies, you'll learn how to finish the year strong and start 2026 with confidence.

Prepare for the Year Ahead

By taking stock of your finances now, you can lay a clear and stable foundation for the new year. Whether your goal is to buy a house, save for retirement, or simply build a more robust emergency fund, a year-end review gives you the clarity needed to create an actionable plan. It’s about being proactive rather than reactive, putting you in control of your financial future. If you’re just getting started, consider reading our blog on Why Young Professionals Should Focus on Building Wealth to help set the right mindset early.

Review Your Bank Accounts and Spending Habits

The first step in any financial check-up is understanding where your money is going. Take a deep dive into your bank statements from the past year. Compare your actual spending against your budget to identify areas where you may have overspent. These "budget leaks" are often small, recurring expenses that add up over time.

Check for Fees, Subscriptions, and Overdrafts

Scrutinize your checking and savings account activity. Are you paying unnecessary bank fees? Have you forgotten subscriptions or auto-renewals for services you no longer use? Identifying and canceling these can free up a surprising amount of cash. Also, keep an eye out for overdraft charges, as they can be a sign that your budget needs re-evaluation.

Replenish Your Emergency Fund

Your emergency fund is a critical safety net. If you had to dip into it during the year for unexpected expenses like car repairs or medical bills, now is the time to focus on rebuilding it. Aim to have at least three to six months of living expenses saved. At Jefferson Bank, we offer a variety of savings account options to help you grow your emergency fund steadily and securely.

Plan for Major 2026 Expenses Now

Life is full of big-ticket expenses: vacations, home repairs, or back-to-school costs. Instead of letting them catch you by surprise, plan for them. By creating a sinking fund for each significant expense, you can save a small amount each month, making these costs much more manageable when they arrive.

Don’t Let the Holidays Undo Your Progress on Debt

The holiday season is filled with emotional triggers that can lead to impulse spending. The desire to give the perfect gift or travel to see loved ones can make it easy to abandon your financial discipline. It's crucial to stay mindful of these temptations and have a plan to avoid taking on high-interest debt.

Budget Before You Buy

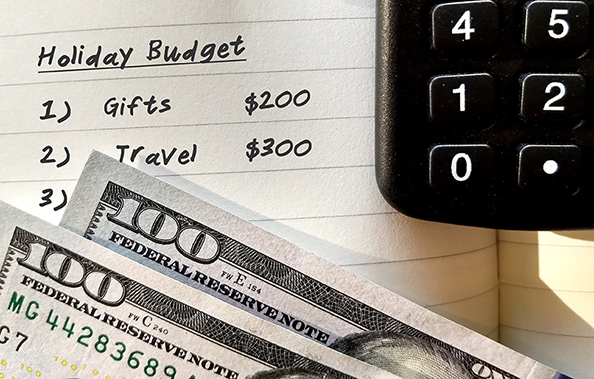

Create a detailed holiday budget that covers everything from gifts and meals to travel and decorations. Look at last year's bank statements to get a realistic idea of what you spent. Allocate a specific dollar amount for each person on your gift list and stick to it. This simple step is one of the most effective ways to prevent overspending.

Avoid Credit Card Traps and Buy Now, Pay Later

While convenient, credit cards and "Buy Now, Pay Later" (BNPL) services can be dangerous if not used responsibly. The high-interest rates on credit card debt can turn a small holiday splurge into a long-term financial burden. If you use credit cards, make a plan to pay the balance in full to avoid interest charges. Be cautious with BNPL services, as they can make it easy to spend more than you can afford. If you’re carrying multiple high-interest balances, consider exploring our personal loan to simplify your payments and free up cash flow.

Redeem Credit Card Rewards to Cover Gifts or Travel

If you have a rewards credit card, the holidays are the perfect time to cash in your points. Redeeming rewards for gift cards, merchandise, or travel can significantly reduce your out-of-pocket expenses.

Holiday Budgeting Tips That Actually Work

Staying on budget during the holidays doesn't mean you have to sacrifice fun. With a few creative strategies, you can celebrate without financial stress.

Adjust Your Monthly Budget Temporarily

To free up cash for holiday expenses, consider temporarily cutting back on non-essential spending. Pause a streaming subscription, dine out less, or reduce your entertainment budget for a month or two. These small sacrifices can make a big difference.

Use Prepaid or Cash-Only Holiday Budgets

A cash-only approach can be a powerful tool for curbing overspending. Withdraw a set amount of cash for your holiday shopping and leave your credit cards at home. When the cash is gone, you’re done spending. A prepaid card can serve the same purpose, helping you stick to a hard limit.

Rethink Traditions That Break the Budget

Traditions are wonderful, but not if they cause financial strain. Suggest new, more affordable traditions with family and friends. Ideas include:

- Secret Santa: Everyone buys one thoughtful gift instead of presents for the whole group.

- Experience Gifts: Pool money for a shared experience, like a weekend trip or a concert.

- Donation Gifts: Make a charitable donation in someone's name.

Stay Organized and Track Spending

Whether you use a budgeting app, a spreadsheet, or a simple notebook, tracking your spending is key. Log every purchase to see where your money is going and ensure you’re staying within your budget.

Debt Payoff Strategies to Reset for the New Year

If you do end the year with some debt, don't despair. Start 2026 with a clear strategy to pay it off and regain control of your finances.

Avalanche vs. Snowball Method

Two popular debt payoff methods are the avalanche and the snowball.

- Avalanche Method: You focus on paying off the debt with the highest interest rate first, while making minimum payments on others. This method saves you the most money on interest over time.

- Snowball Method: You focus on paying off the smallest debt first, regardless of the interest rate. The quick win of eliminating a debt provides motivation to keep going.

Jefferson Bank offers a free budgeting spreadsheet to help you get started budgeting.

Consider Consolidation or Refinance

If you have multiple high-interest debts, consolidating them into a single loan with a lower interest rate could be a smart move. A personal loan or home equity loan can simplify your payments and reduce the total interest you pay. Talk to a financial advisor to see if this is a good option for your situation.

Don’t Pause Retirement Contributions if You Can Help It

While it can be tempting to pause retirement savings to pay off debt faster, it's important to find a balance. If your employer offers a 401(k) match, contribute at least enough to get the full match; it’s free money. Then, you can direct any extra funds toward your debt.

Year-End Investment, Tax & Retirement Moves to Consider

For those looking to further optimize their financial strategy, the end of the year is a prime time for some advanced moves.

- Rebalance Your Portfolio: Review your investment portfolio to ensure it’s still aligned with your risk tolerance and long-term goals.

- Harvest Tax Losses or Gains: Sell investments at a loss to offset capital gains and potentially reduce your tax bill.

- Max Out Your 401(k) or IRA: If you can, contribute the maximum amount to your retirement accounts to take full advantage of tax benefits.

Take Your RMDs: If you are over 73, you must take Required Minimum Distributions (RMDs) from your retirement accounts by year-end to avoid penalties.

Create Financial Goals That Stick in 2026

With your finances reviewed and your holiday spending managed, it’s time to look ahead.

Document Major Life Changes

Did you get a new job, get married, or have a baby? Major life changes can have a significant impact on your finances. If you’re updating your estate or long-term plans, read our blog on Why You Should Use a Corporate Fiduciary for Your Estate Planning to understand how a professional fiduciary can help manage assets responsibly.

Set SMART Financial Goals for 2026

The best goals are SMART: Specific, Measurable, Achievable, Relevant, and Time-bound. Instead of a vague goal like "save more money," set a specific goal: "Save $5,000 for a down payment by December 2026 by automatically transferring $417 from my checking to my savings account each month."

Year-End Financial Checklist FAQs

What should be on a year-end financial checklist?

A year-end financial checklist should include reviewing your spending habits, assessing savings and emergency funds, paying down high-interest debt, reviewing your investment portfolio, maximizing retirement contributions, checking insurance coverage, and setting new financial goals for the year ahead.

How can I avoid holiday debt?

Start with a realistic holiday budget and stick to it. Track every purchase, avoid impulse buys, and use credit card rewards or cash-back apps where possible. Consider low-cost gifts like handmade items, experiences, or a Secret Santa exchange to reduce spending.

Should I use my emergency fund for holiday spending?

No. Your emergency fund is for unexpected situations like medical bills, car repairs, or job loss. Instead, adjust your regular budget or scale back holiday spending to avoid dipping into savings.

What’s better for paying off debt: avalanche or snowball method?

Both work well. The avalanche method saves more on interest by targeting high-rate debts first. The snowball method builds momentum by paying off smaller balances first. Choose the one that keeps you motivated.

Can I use credit card rewards to buy holiday gifts?

Redeeming rewards points for gift cards or travel can ease holiday expenses. Just avoid overspending to earn points and make sure you pay your balance in full to avoid interest charges.

Jefferson Bank Is Here to Help You Finish the Year Strong

Navigating your finances can feel overwhelming, but you don't have to do it alone. At Jefferson Bank, we believe in building long-term, personal, relationships to help our community thrive. From our budgeting spreadsheet to our personal financial management tool in online banking, Our local experts here to ensure you finish the year strong and start the new year with financial confidence. Let Jefferson Bank be your guide to a brighter financial future.